Most people who start investing make the same mistake in the first six months: they pick assets they understand emotionally, not financially. A rental property in their hometown because it feels safe. Index funds because someone on a podcast said so. Gold because the news scared them. By the time they finally stop to consider how everything connects—if they ever do—they have already built the portfolio backwards.

Asset allocation is not glamorous. It does not promise you will double your money in a year. That is not its purpose. Asset allocation is the single most important decision you make as an investor. It matters more than stock selection, more than timing, and more than which brokerage you use. Research by Vanguard and others shows that asset allocation drives over 90% of long-term portfolio return variability, not the specific assets investors choose within each category.

That number surprises people. It should not.

What Asset Allocation Actually Means

At its core, asset allocation means deciding how much of your money goes into different categories. The main categories include equities (stocks), fixed income (bonds), real assets (property and commodities), and cash. Each category behaves differently under different economic conditions. When stocks fall sharply, bonds often hold steady or rise. When inflation spikes, real assets tend to do better than cash. The point is not to predict what will happen next — nobody does that reliably. The point is to build a portfolio that does not collapse entirely under any single scenario.

This is where most beginners get it wrong. They treat allocation like a one-time event. They pick a percentage split, buy the assets, and assume the job is done. In reality, allocation drifts constantly as market prices move. A portfolio that started at 60% equities and 40% bonds in early 2020 looked very different by late 2021. If you never rebalance, what you think you own and what you actually own diverge significantly over time.

The other common error is conflating asset allocation with diversification. They are related but not the same thing. You can own thirty different stocks and still have a poorly allocated portfolio. All of them sit in the same asset class. When markets get rough, they tend to move together. True allocation spreads risk across categories that respond differently to the same economic pressures.

The Myth of the “Right” Allocation

Many investors treat the 60/40 portfolio — 60% stocks and 40% bonds — as the universal benchmark for sensible investing. Financial planners have used it as a default for decades, and for a long time it worked reasonably well. The 2022 calendar year exposed its limits. Both stocks and bonds fell simultaneously, something that historically had been uncommon. A 60/40 investor lost money on both sides of their supposed hedge.

This does not mean the 60/40 approach is permanently broken. It means it was never a law — it was a heuristic that worked under specific conditions: falling interest rates and low inflation. When those conditions changed, so did the performance. Any beginning investor who was told “just do 60/40 and forget it” received incomplete advice.

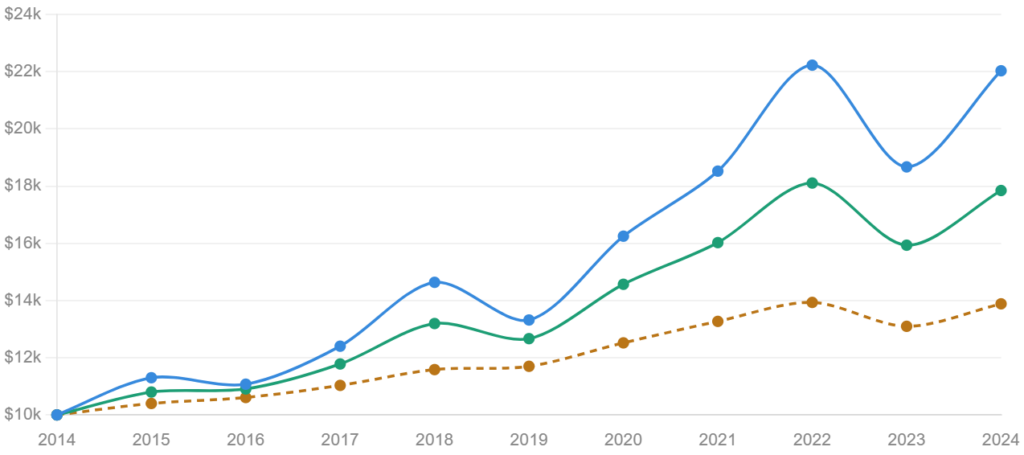

The chart below compares three allocation profiles over a volatile decade. It includes an aggressive equity-heavy portfolio, a balanced mix, and a conservative bond-heavy approach. The aggressive portfolio finishes with the highest return, but the ride is much rougher. In any two- or three-year window, the results are much closer than the long-term gap suggests.

What the chart also shows — though people rarely talk about it — is how much 2022 hurt every type of investor. The aggressive portfolio dropped sharply, but even the conservative one gave back ground. No allocation is immune to a year when both major asset classes move in the same direction. The difference is how quickly each profile recovers, and how much sleep you lose in the process.

The Three Factors That Should Drive Your Allocation Decision

Before copying someone else’s allocation, there are three things worth understanding about your own situation. Most advice skips these and jumps straight to percentages.

1. Time horizon

This is the single most important variable. An investor with 30 years before they need the money can absorb a 40% portfolio drawdown and still recover fully. An investor who needs funds in five years cannot. A heavy equity allocation that is entirely rational for a 30-year-old becomes genuinely reckless for a 58-year-old approaching retirement.

The mistake I see repeatedly is people applying long-horizon thinking to short-horizon goals. Someone saving for a house deposit in three years should not have 80% of that money in stocks. If the market drops 35% in year two, they miss their purchase window or they buy anyway. Either way, they start homeownership with a depleted financial cushion.

2. Risk tolerance — real, not theoretical

Every brokerage questionnaire asks some version of “how would you feel if your portfolio dropped 20%?” Most people answer as if they are calm, rational investors who would simply stay the course. Then the market actually drops 20%, and they sell everything at the bottom.

Real risk tolerance is revealed in behavior, not questionnaires. If you have never held a portfolio through a genuine downturn — the kind where your balance drops by $30,000 or $50,000 in a matter of weeks — you do not actually know your risk tolerance. Be honest about this. It is better to accept a slightly lower long-term return with an allocation you will actually hold through volatility than to own an “optimal” allocation you will abandon at the worst possible moment.

3. Income stability and liquidity needs

A salaried professional with predictable income and six months of cash reserves can afford to have most of their investable money in illiquid or volatile assets. A self-employed person with irregular income, or someone supporting dependents on a single income, needs to carry more conservative allocations — not because the returns are better, but because unexpected life events can force you to sell assets at exactly the wrong time.

This is where property as an asset class requires particular care. Real estate is illiquid almost by definition. If you have most of your net worth tied up in property and a rental property sits vacant for six months in a downturn, you may find yourself forced to sell other assets — or worse, miss mortgage payments — because you cannot access your equity quickly. Liquidity is part of allocation thinking that rarely gets discussed.

How to Actually Build Your First Allocation

There is no formula that works for everyone, but there are principles worth following.

Start with your equity percentage. A commonly used rule of thumb is to subtract your age from 110 to get your equity allocation. A 30-year-old would hold 80% in equities, a 50-year-old would hold 60%. This is a starting point, not a conclusion. Adjust upward if you have a long horizon, stable income, and high genuine risk tolerance. Adjust downward if any of those conditions are missing.

Within equities, think about geographic spread. Concentrating entirely in your home country’s stock market exposes you to that country’s specific economic and political risks. Most experienced investors spread equity exposure across domestic, international developed markets (US, Europe, Japan), and a smaller allocation to emerging markets. The proportions vary, but the principle holds: single-country equity concentration is a hidden risk that many beginner portfolios carry without realizing it.

Within fixed income, think about duration and credit quality. Short-duration government bonds are very different from long-duration corporate bonds. In a rising interest rate environment — which most developed markets experienced between 2022 and 2024 — long-duration bonds fell sharply in price. Many investors who held bond funds expecting stability were surprised to see significant losses. Understanding what you own inside each category matters almost as much as the category allocation itself.

Real assets — property, infrastructure, commodities — serve as inflation hedges. They do not always move with stocks and bonds, which is their value. But they come with their own complexities: property requires management and capital, commodities can be extremely volatile, and infrastructure investments are often only accessible through funds with their own fee structures. For most beginners, a 5–15% allocation to real assets is a reasonable place to start, often accessed through REITs or commodity ETFs rather than direct ownership.

Cash and cash equivalents — money market funds, short-term Treasury bills — are often undervalued by beginning investors focused on returns. Holding some cash gives you the ability to buy other assets when they fall sharply. It also protects you from forced selling in a downturn. The “cost” of holding cash is the return you give up on that portion, which at current rates is lower than it was in the near-zero interest rate era of 2010–2021.

When a Sound Allocation Strategy Still Fails

This is the section most guides leave out. A well-constructed allocation can still produce poor outcomes under specific circumstances.

The most common failure mode is abandonment. An investor builds a sensible 70/30 portfolio, holds it for two years, watches equities fall during a correction, and switches to something more conservative at exactly the wrong moment. They lock in losses, miss the recovery, and end up worse off than if they had held a more conservative portfolio consistently from the start. Switching allocation in response to short-term performance is almost always a mistake, and yet it is the most common investor behaviour during downturns.

The second failure mode is fees. A well-constructed allocation spread across actively managed funds with expense ratios of 1.5–2% per year will underperform a simpler allocation of low-cost index funds over most long-term periods. The mathematics are unforgiving: a 1.5% annual fee compounds against you just as relentlessly as returns compound for you. Over 20 years, the difference between a 0.15% expense ratio and a 1.5% expense ratio on a $100,000 portfolio can exceed $80,000 in terminal value. The allocation itself becomes almost irrelevant if the fee drag is large enough.

The third failure mode is ignoring taxes. In the UK, investments held outside an ISA are subject to capital gains tax and dividend tax. Meanwhile, in the US, taxable accounts face short- and long-term capital gains taxes depending on the holding period. In Canada, only 50% of capital gains are included in taxable income, but contribution room in registered accounts like RRSPs and TFSAs is limited. A portfolio that looks efficient in gross return terms can look very different after accounting for tax drag. Placing higher-returning, higher-turnover assets inside tax-advantaged wrappers where available is part of allocation strategy that most beginner guides ignore entirely.

Rebalancing: The Part Everyone Skips

If you do nothing else, rebalance. Rebalancing means periodically resetting your portfolio back to its target allocation percentages. If equities have a strong year and now represent 75% of your portfolio instead of your target 65%, rebalancing means selling some equities and buying more of whatever has lagged.

This feels counterintuitive. You are selling what has gone up and buying what has gone down. But that is precisely what makes it effective — it enforces a buy-low, sell-high discipline that is otherwise almost impossible to maintain emotionally.

Most investors rebalance either on a calendar schedule (once or twice per year) or when an asset class drifts more than a set threshold from its target — say, 5 percentage points. Both approaches work. What does not work is rebalancing too frequently, which generates transaction costs and potential tax events without meaningfully improving outcomes, or not rebalancing at all, which leaves your allocation drifting wherever markets take it.

There is one practical consideration that matters here: rebalancing in tax-advantaged accounts (ISAs, 401ks, RRSPs, SIPPs) has no immediate tax cost. Rebalancing in taxable accounts generates taxable events. Where possible, direct new contributions toward underweight asset classes first — this rebalances the portfolio without triggering sales and the associated tax implications.

What a Realistic Beginner Portfolio Might Look Like

Rather than prescribe specific funds, it is more useful to think in terms of a framework. A beginner investor in their late 20s or 30s with a stable income, a long time horizon, and genuine (not theoretical) comfort with volatility might reasonably consider something in the range of 70–80% equities, 10–15% bonds, 5–10% real assets, and 5% cash. That is not a recommendation — it is an illustration of how these categories might be weighted given those specific circumstances.

Someone in their 50s approaching retirement might look at 45–55% equities, 30–35% bonds, 10% real assets, and 10% cash. Again, individual circumstances change everything. Someone with a defined benefit pension already in place effectively has a large fixed income component in their overall financial picture, which changes what they need from their investable portfolio.

The allocation that works is the one you understand well enough to hold through a difficult year.

Frequently Asked Questions

Q: How often should I change my asset allocation? Major allocation shifts should be driven by genuine changes in your life circumstances — a significant change in time horizon, income stability, or financial goals — not by market conditions. Gradual shifts over time are expected, particularly as you approach retirement. Reacting to short-term market performance by changing allocation is almost always a decision you will regret within a few years.

Q: Is property a replacement for other asset classes? Not straightforwardly. Property offers inflation protection, potential income, and long-term capital appreciation — but it is illiquid, concentrated in a single geography, requires active management, and has significant transaction costs. Treating a rental property as your entire real asset allocation is reasonable, but assuming it covers your equity and bond allocation is a category error. Property does not behave like stocks or bonds, and it should not be counted as a substitute.

Q: Should I hold bonds if interest rates might rise? Rising rates hurt bond prices, particularly long-duration bonds. But bonds still serve a role in reducing overall portfolio volatility, particularly short-duration or inflation-linked variants. Rather than abandoning bonds entirely, consider their duration carefully. Short-duration bonds are far less sensitive to rate movements than long-duration ones. The question is not whether to hold bonds, but which bonds.

Q: Does asset allocation still matter in a low-return environment? More than ever. When returns are compressed across all asset classes, the cost of being in the wrong one at the wrong time is proportionally higher. In a high-return environment, poor allocation is masked by broad market tailwinds. When expected returns are modest, the drag from misallocation or high fees becomes the dominant factor in outcomes.

Q: How do I handle allocation if I also own investment property directly? Count it. Direct property is a real asset and should be included in your overall picture. If your investment property represents 60% of your net worth, your financial portfolio needs to complement that concentration, not ignore it. That likely means reducing your weighting in real estate funds or REITs within the portfolio and ensuring you have adequate liquidity elsewhere to weather vacancy periods or unexpected repairs.

Q: Is there a minimum portfolio size where allocation starts to matter? Below around $10,000–$15,000, transaction costs and the limited divisibility of assets make precise allocation difficult to implement. At smaller portfolio sizes, a single broad global equity index fund is a sensible starting point. Focus on building the portfolio to a size where allocation becomes practical, rather than optimizing a percentage split across six categories with $5,000. The habits of thinking about allocation, however — time horizon, risk tolerance, liquidity needs — are worth developing from the beginning regardless of portfolio size.

Before making any allocation decision, check what you already own across all accounts, not just the one you are currently managing. Many investors are surprised to find their overall allocation is far more concentrated in equities — or in their home market — than they realized once they count everything together. Start there. Then decide what your genuine time horizon is and how you have actually behaved in previous downturns, not how you think you would behave. The gap between those two answers is usually where the real allocation decision lives.

[…] The mechanical investor doesn’t question this. The experienced investor starts to wonder whether the rules are actually serving them. […]

[…] does not matter whether the account is currently open. Former account holders who closed years ago are still included. The only question is whether you held a 360 […]