Most people who set out to build a million-dollar property portfolio never get there. Not because they lacked ambition or capital. A few early structural decisions quietly compounded into dead ends. They may have bought the wrong property type for their tax position. Or they scaled too quickly into markets that looked strong on paper. In reality, those markets behaved very differently.

This isn’t a motivational roadmap. It’s a practical breakdown of how a real estate portfolio grows from one property into a valuable asset base.

It also shows where that process breaks down for most investors. Many people try it. Fewer execute it successfully.

Read more :How to Build Multiple Income Streams from Scratch

What “A Million-Dollar Portfolio” Actually Means

Before anything else, let’s get specific about language. A million-dollar portfolio could mean you own properties with a combined market value of $1 million. It could also mean you’ve built a million dollars in net equity after debt. These are very different financial positions.

An investor who owns five properties collectively worth $1.2 million but carries $950,000 in mortgages has a net position of $250,000. That’s not nothing — but it’s also not what most people picture when they use the phrase “million-dollar portfolio.”

The cleaner definition — and the one worth working toward — is $1 million in unencumbered equity across your holdings. That number gives you real leverage, real borrowing power, and genuine financial flexibility. Chasing total asset value inflates the ego more than the balance sheet.

Why the First Property Matters More Than Most Investors Realize

The first property isn’t just a purchase. It sets the financial pattern for everything that follows. The mortgage structure, the rental yield, the property type, the location’s growth trajectory — all of these create either momentum or drag for the next acquisition.

This is where most investors go wrong. They treat the first purchase as a test run and assume they can correct course later. But the first property sets the foundation. If it locks capital into a low-yield asset in a flat market, problems start early. Borrowing capacity for the second property becomes limited quickly. The bank doesn’t care about your vision. They care about your current debt-to-income ratio and the rental income your existing property actually generates.

A property that rents for $1,400 per month in a market where comparable yields are $1,800 isn’t just underperforming today — it’s reducing what you can borrow tomorrow.

For the first property, prioritize:

Rental yield over projected appreciation. Cash flow funds future purchases; appreciation is a bonus, not a strategy. Focus on a market with genuine rental demand, not speculative investor demand. Choose a property type with low maintenance unpredictability — avoid older buildings with aging infrastructure unless you have deep reserves. And structure your financing so you can survive if rates move two percentage points higher.

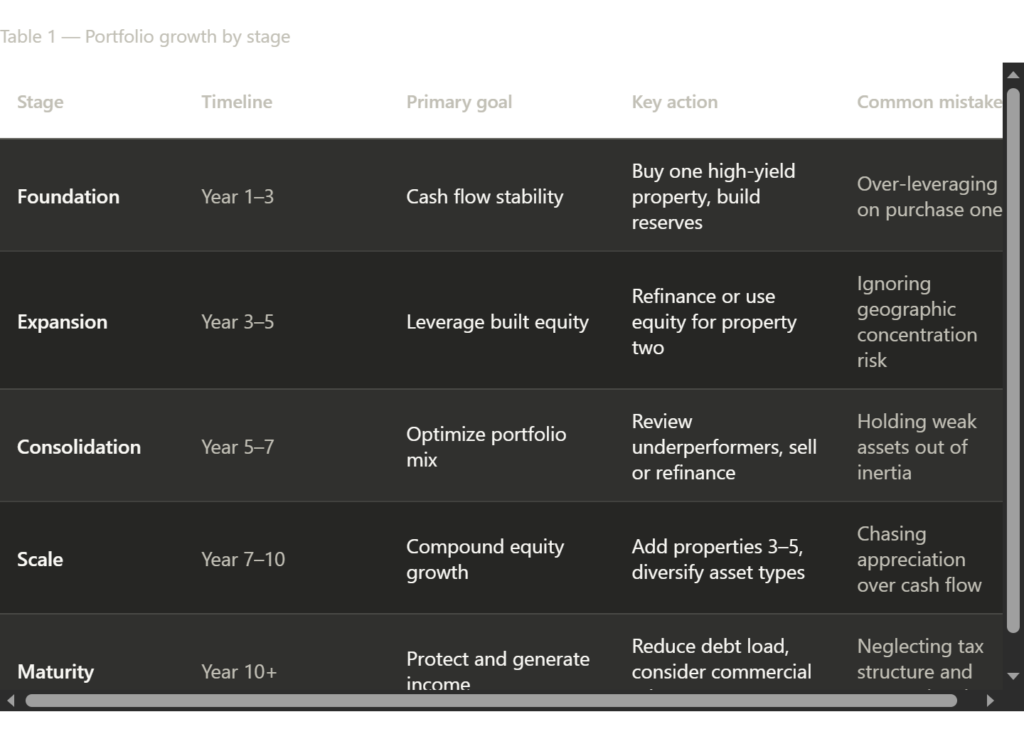

The Scaling Logic That Actually Works

There’s a common belief that scaling a portfolio is simply about buying more properties. In practice, the investors who reach meaningful portfolio size do so through a fairly deliberate sequence — not aggressive accumulation.

The pattern above isn’t a guarantee — it’s a framework. In practice, each stage can be compressed or extended depending on market conditions, your income profile, and how aggressively you’re able to deploy capital. What matters is that each stage has a distinct purpose. Mixing them up — trying to scale in year two before the first property is stable — is how investors end up cash-strapped when rates rise or a tenant vacates.

Cash Flow Versus Appreciation: The Debate That Trips Up Most Investors

There’s a persistent myth in real estate circles that appreciation is the primary wealth-builder and rental income is just a nice bonus. In certain markets during certain periods, that’s been true. But as a deliberate investment strategy, banking on appreciation is closer to speculation than investing.

Here’s the problem: appreciation is retrospective. You can study historical price trends, overlay infrastructure spending, analyze population inflows — and still be wrong about a specific market over a five- to seven-year holding period. Cash flow, on the other hand, is measurable before you close. It’s either there or it isn’t.

This doesn’t mean appreciation markets should be avoided. It means they require a different financial structure. If you’re buying in a market where gross yields are 3.5% because you believe values will climb 40% over the next decade, you need to be able to carry that property through vacancy periods, rate increases, and soft patches without selling under pressure. Most individual investors can’t. They run out of reserves and sell at exactly the wrong time.

The investors who genuinely accumulate wealth through real estate tend to do so through compounding yield over long holding periods — not timing markets.

The Financing Structure Nobody Talks About Enough

Financing is where the real mathematics of a property portfolio actually come into play, yet investors often discuss it far less than property selection.

Two investors buy identical $400,000 properties in the same suburb. One structures a 25-year amortization at a fixed rate for five years. The other takes a variable rate product with an interest-only period. Over three years, the second investor shows better monthly cash flow — but when rates shift or the interest-only period ends, the payment structure changes significantly and the refinancing options narrow.

Fixed-rate mortgages cost more monthly but create predictability. Variable products offer better short-term cash flow but transfer rate risk to the borrower. Neither is universally wrong. What matters is whether the financing structure matches your holding timeline and your ability to absorb payment shocks.

This is where I wouldn’t take a variable rate product unless I had significant liquid reserves and a clear exit or refinancing strategy within 24 months. If neither of those conditions applies, the slightly higher monthly cost of fixed financing is an insurance premium worth paying.

When This Strategy Fails

A million-dollar portfolio is not a passive outcome.There’s a version of this story where an investor ends up with five properties, all negatively geared. Rental income isn’t enough to cover repayments during a cluster of vacancies.

That scenario is most likely when:

The investor overpays for properties during a competitive market and locks in thin margins that disappear when maintenance costs rise. Or they concentrate their holdings in one city that later suffers an economic shock. A major employer may leave, or policy changes can reduce rental demand. Others fail to keep enough cash reserves. This can force them to sell during a downturn just to cover shortfalls elsewhere in the portfolio.

A portfolio that looks healthy in a rising market can become a liability in a flat or declining one. The properties themselves don’t change — but the financing costs, the ability to refinance, and the rental demand environment all shift. Real estate is not liquid, and that illiquidity cuts both ways.

Busting Two Common Portfolio-Building Myths

Myth one: “Buy as many properties as possible as fast as possible.”

This advice circulates in investment communities as if speed is the primary variable. It isn’t. Portfolio velocity without cash flow discipline creates fragile structures. The investors who scale fastest are often the most exposed during rate cycles or economic corrections. Stable, deliberate accumulation almost always outperforms aggressive acquisition over a 15-year horizon.

Myth two: “Location is everything.”

Location matters, but it’s not sufficient. A well-located property in poor physical condition, with structural issues, aging plumbing, or outdated electrical systems, generates maintenance costs that quietly erode yield for years. An investor who pays a slight premium for a newer property in a slightly less prestigious suburb often outperforms on net cash flow over a five-year period. Location shapes appreciation potential. It doesn’t guarantee it, and it doesn’t substitute for property fundamentals.

The Tax Layer That Determines Real Returns

Real estate returns are pre-tax numbers until they aren’t. In the US, UK, and Canada, the tax treatment of rental income, capital gains, and depreciation differs significantly — and those differences materially affect your net position.

In the United States, investors can depreciate residential property over 27.5 years, creating a valuable tax shield that reduces the amount of rental income subject to tax. Meanwhile, the United Kingdom has steadily scaled back mortgage interest relief for landlords since 2017, a change that has hit highly leveraged, higher-income investors particularly hard. By contrast, Canada taxes rental income as ordinary income, yet only 50% of capital gains are taxable, which often encourages investors to think carefully about the most efficient ownership structure.

I wouldn’t build a multi-property portfolio without a tax professional who specializes in real estate investment. The decisions made at purchase — whether to hold in personal name, a partnership, or a corporation — have compounding tax implications that are very difficult to reverse. Getting this right early saves more than most investors realize.

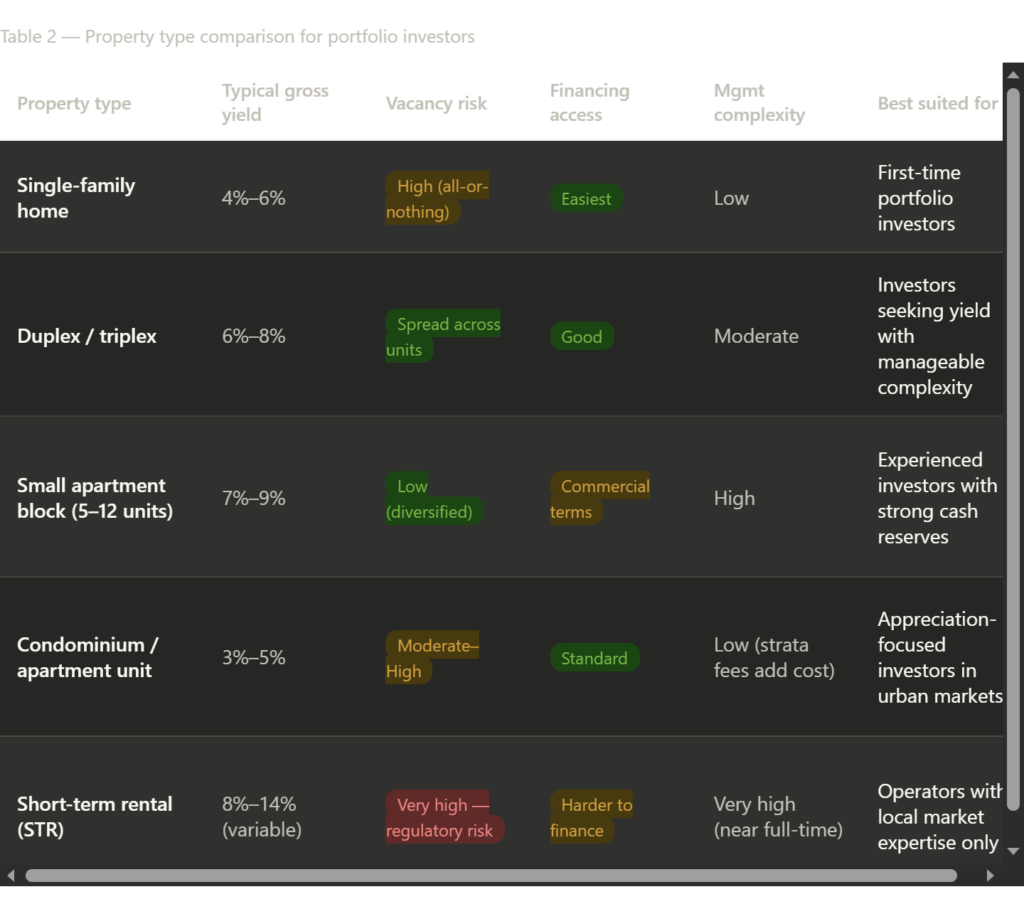

Property Types and What They Actually Mean for Your Portfolio

Not all residential property is equivalent as a portfolio asset. Single-family homes, small multifamily units, and apartment buildings behave differently across cash flow, vacancy risk, management complexity, and financing access.

Single-family homes get most of the attention in beginner investment discussions, but small multifamily units — duplexes and triplexes — often represent better risk-adjusted returns for portfolio builders. The vacancy risk is distributed across units, the financing structures are still accessible to individual investors, and the management complexity, while higher than a single house, doesn’t require dedicated property management until you’re at scale.

Short-term rentals are a separate category entirely. The gross yield numbers look compelling, but the management burden is substantial, and the regulatory environment in most major cities is tightening. Cities like New York, London, and Toronto have implemented registration requirements and cap limits on short-term rental nights. An investment thesis built on short-term rental income in an urban market carries regulatory risk that a standard buy-to-let doesn’t.

What “Market Research” Actually Means Before You Buy

Investors often say they’ve done their research when they’ve checked median property prices and looked at one or two local rental listings. That’s a start, but it doesn’t tell you what you need to know before committing six figures.

The metrics that actually matter before purchase: gross rental yield compared to suburb average, days on market for comparable properties (this tells you demand depth), vacancy rates at the suburb level, the ratio of owner-occupiers to renters (high renter concentrations can mean more transient tenant pools), and any major infrastructure or employer changes planned or underway in the area.

Government planning portals, local council zoning documents, and state-level housing supply data are more useful than most commercial property research platforms. Relevant government resources in the US include the Census Bureau’s rental vacancy data and HUD’s fair market rent figures. In the UK, the ONS private rental market statistics provide regional context. In Canada, CMHC’s rental market reports are published quarterly and broken down by metropolitan area.

None of this research eliminates risk. It reduces the probability of an unpleasant surprise in year two of ownership.

Reserve Levels Most Investors Underestimate

The standard advice is to hold three to six months of expenses in reserve per property. In practice, that’s the minimum, not the target — and it assumes your properties are relatively new, your tenants are stable, and you’re not carrying significant leverage.

For a portfolio of three or more properties, a more realistic reserve is equivalent to six months of total mortgage payments plus a dedicated maintenance fund of one to two percent of property value annually. On a $400,000 property, that’s $4,000–$8,000 per year set aside purely for maintenance. Older properties and those with high-wear components like roofing, HVAC systems, or plumbing push toward the higher end.

Investors who don’t maintain adequate reserves tend to make poor decisions under pressure. They accept below-market tenants to fill a vacancy quickly, or they defer maintenance that compounds into larger structural issues. Both erode long-term asset value.

The Point at Which Professional Management Makes Sense

Self-managing two properties is manageable for most investors who are organized and available. At three or more properties — especially across different locations — the management burden starts to compete with the time and attention required for acquisition due diligence and financing.

Professional property management typically costs 8–12% of gross rental income. On a $1,800 monthly rent, that’s $144–$216 per month per property. Most investors resist this cost, viewing it as pure margin erosion. But what it buys is documented compliance, consistent rent collection practices, faster vacancy fills through established tenant networks, and documented maintenance records that are valuable at refinancing.

I wouldn’t manage more than three properties entirely on my own unless property management was my primary occupation. The margin savings don’t justify the opportunity cost of time that could be spent on acquisition, financing, and tax planning.

What to Check, What to Avoid, and What to Decide Next

Before adding your next property, verify the gross yield against the local market average — not the asking price projections from the listing agent. Run the cash flow calculation at your actual financing rate, not the promotional rate you’ve been quoted. Check the vacancy history for the suburb over the past three years, not just the current tight market.

Investors should be cautious of markets where the entire strategy relies on future price growth rather than solid fundamentals. Property types that demand daily, hands-on management can also become overwhelming without the right systems and team in place. Financing structures deserve equal attention, and any loan with features you don’t fully understand should be approached with extreme care.

The decision most investors at the early stage need to make isn’t which property to buy next — it’s whether the one they already own is actually performing the way they thought it would. If it isn’t, understanding why tells you far more about how to build the next stage of the portfolio than any market research will.

A portfolio that reaches genuine seven-figure equity is usually built over 10–15 years, through a combination of deliberate acquisitions, disciplined financing, tax-aware structuring, and the patience to hold quality assets through short-term market noise. The investors who make it there rarely did so by taking outsized risks. They did it by avoiding the structural mistakes that erode the compounding process.

Frequently Asked Questions

How much capital do I realistically need to start building a portfolio?

The practical minimum in most US, UK, and Canadian markets is enough to cover a 20–25% deposit on an investment property, plus three to six months of reserves, plus transaction costs. In many mid-tier markets, that means $60,000–$100,000 to start responsibly. Investors who stretch to buy with lower deposits face higher monthly financing costs and reduced borrowing power for subsequent acquisitions. Starting with adequate capital is not optional — it shapes the entire trajectory.

Is it better to own five small properties or one larger multifamily building?

There’s no universal answer. Five small properties give you geographic diversification and the option to sell individual assets for liquidity. One larger multifamily building gives you economies of scale in management and typically better per-unit yield. The right structure depends on your management capacity, financing access, and whether your primary goal is monthly income or long-term equity accumulation. Most individual investors are better served by the distributed approach until they have the experience and reserves to manage a larger commercial asset.

How do rising interest rates affect a portfolio growth strategy?

Significantly, and in multiple ways. Higher rates increase monthly carrying costs, compress cash flow margins, and reduce the refinancing value of existing properties. They also tend to cool overall market prices, which can create acquisition opportunities if you have access to capital. The investors most affected by rate cycles are those who acquired aggressively at low rates and are now holding properties with thin margins that can’t absorb increased financing costs. A portfolio designed for resilience should function acceptably at rates two percentage points above current levels.

Should I hold properties in a personal name or a corporate structure?

The right ownership structure varies based on jurisdiction, income level, and long-term investment goals. In the United States, holding property through an LLC can provide liability protection, but the tax outcome depends on how the entity is classified for tax purposes rather than the LLC itself. Across the United Kingdom, the corporate landlord model has grown more appealing since restrictions on individual mortgage interest relief were introduced, although it brings additional complexity around corporation tax and dividend extraction. Meanwhile, in Canada, owning rentals personally may preserve access to the principal residence exemption for one property and can avoid extra corporate tax layers for smaller portfolios. Seeking jurisdiction-specific professional advice is essential before choosing a structure.

What’s the most common reason investors stall before reaching their portfolio goals?

Cash flow problems, almost universally. Either the first or second property wasn’t yielding enough to support the borrowing required for the next acquisition, or the investor hadn’t maintained reserves and was forced to pause after an unexpected maintenance event or vacancy. The investors who scale consistently are those who treat cash flow margin as non-negotiable on every acquisition — even when a low-yield, high-appreciation property appears more exciting.

Is this realistic for someone who isn’t a full-time investor?

Yes, but only if expectations about pace are realistic. A portfolio of three to five well-selected properties managed with professional help doesn’t require full-time attention. What it requires is disciplined initial decision-making — the right property types, the right financing structures, adequate reserves, and a tax-aware holding structure from the start. Most of the meaningful work happens at acquisition and at the annual review. The day-to-day can be delegated. The strategic decisions cannot.

[…] Read more :How to Build a Million-Dollar Real Estate Portfolio Step-by-Step […]

[…] who are significantly behind, time in the market usually matters more than choosing the perfect tax-advantaged vehicle. The right account still matters, but investing today in any available account beats waiting to […]