")

Most people come to ETF investing with a mental image of sitting back and watching dividends roll in. That picture isn’t entirely wrong — but the version they’ve imagined rarely survives contact with reality. A 4% yield sounds attractive until you realize many funds eroding their own value to maintain it.. That’s not income. That’s your principal dressed up as a dividend check.

ETF investing for passive income can genuinely work. But it works on specific terms that most beginner guides skip over, either to keep things simple or to avoid scaring people off. This piece won’t do that. If you’re here to learn how to build a realistic income stream from ETFs, you need to understand both sides of the trade.

How to Build a Diversified Portfolio with Little Money

What “Passive Income” From ETFs Actually Means

The phrase passive income is used so loosely it has lost most of its meaning. In the context of ETFs, income comes from two places: distributions (dividends from underlying stocks or interest from bonds) and, for some strategies, premium income from options (as with covered call ETFs). That’s it. There is no mechanism inside an ETF that generates money from nothing.

When an ETF pays a dividend, one of three things is happening. The underlying companies are genuinely profitable. The fund is returning interest from bonds or REITs. Or — and this is where beginners get hurt — it’s paying out your own money repackaged as income.

That last scenario is disturbingly common in high-yield ETF categories. A fund yielding 10–12% annually is manufacturing that number. The cost usually shows up in a declining share price over time. You’re not earning income; you’re slowly liquidating your position in monthly installments.

This is where most investors get it wrong: they evaluate ETFs by yield percentage alone, without asking where that yield is actually coming from.

The Core ETF Income Categories and What They Really Deliver

Dividend equity ETFs

These hold stocks of companies with established dividend-paying histories. Funds tracking indices like the S&P 500 Dividend Aristocrats, the FTSE All-World High Dividend Yield index (relevant for UK and Canadian investors), or sector-specific dividend payers in utilities and consumer staples are the cleanest version of this strategy.

Yields typically range from 2% to 4.5% annually, depending on market conditions and interest rate environment. That might not sound exciting, but the dividend payments from well-run underlying companies tend to be sustainable, and share price appreciation can run alongside them.

The honest trade-off: you’re accepting a lower yield in exchange for lower distribution risk. In rising rate environments like 2022 to 2024 dividend ETFs often underperform bonds on pure income, even while staying more stable than growth funds.

How to Find Undervalued Stocks Using Free Tools

Bond ETFs

Government bond ETFs and investment-grade corporate bond ETFs pay interest distributions based on the yields of the underlying debt instruments. In periods of higher interest rates, these have become genuinely competitive income vehicles. US Treasury ETFs, UK Gilt funds, and Canadian government bond ETFs were delivering 4%–5% yields as recently as late 2023 and into 2024, which was unusual by historical standards.

The risk most beginners underestimate with bond ETFs is duration. A long-duration bond ETF (holding bonds maturing in 15–30 years) is highly sensitive to interest rate changes. When rates rise, long-duration bond ETF prices fall significantly. You can be earning a 4% distribution while watching your capital value drop 10–20%. This is not a hypothetical — it happened to investors in popular long-duration bond ETFs between 2021 and 2023.

Short-duration bond ETFs carry much less price volatility and are a more sensible starting point for income-focused beginners.

Covered call ETFs (and what they don’t tell you upfront)

Covered call ETFs — sometimes marketed as “enhanced income” funds — generate premium income by selling options contracts against the underlying holdings. In stable or slightly declining markets, these can produce high distribution yields, sometimes 8–12% annually.

Here’s what the marketing glosses over: when markets rise sharply, covered call ETFs cap your upside. The options sold obligate you to give up gains beyond the strike price. In a strong bull market, a covered call ETF on a major index will dramatically underperform the plain index ETF. You trade long-term capital growth for short-term income, and that trade-off is permanent as long as you hold it.

I wouldn’t use covered call ETFs as a core holding for anyone under 55 with a 15+ year investment horizon. For someone in or near retirement who prioritizes income over growth, it’s a different conversation.

Building a Realistic Income Portfolio With ETFs

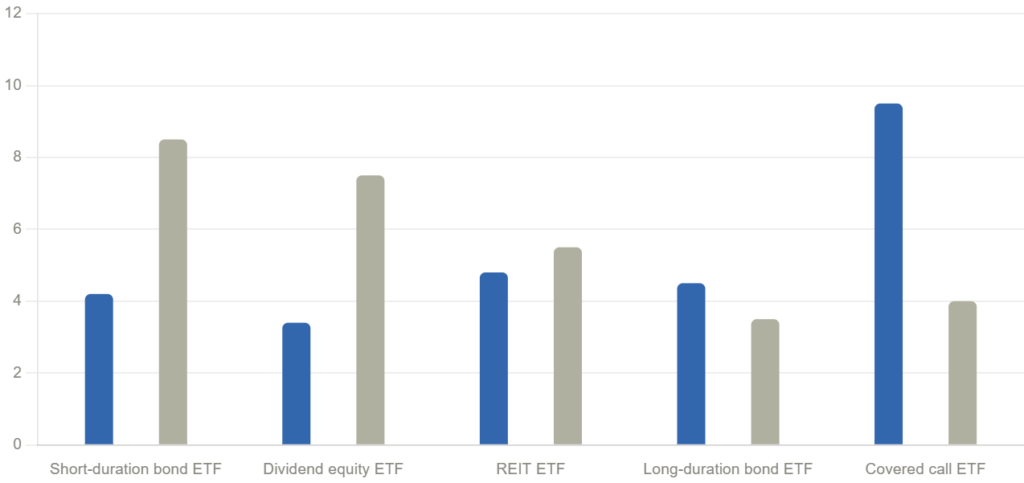

The chart below illustrates how different ETF income strategies have historically compared in terms of yield versus capital stability — two factors that rarely align perfectly.

Notice that the highest-yielding option on the chart — covered call ETFs — carries one of the lowest capital stability scores. This is not a coincidence. The relationship between yield and capital risk is almost always inverse in the ETF income world. When you see a fund offering double the yield of its peers, the question to ask immediately is: what is this fund doing that the others aren’t, and what am I giving up in return?

A functional income ETF portfolio usually combines two or three categories rather than committing to one. A reasonable beginner split: 50% in a dividend equity ETF, 30% in a short-to-medium bond ETF, and 20% in a REIT ETF for real estate exposure. This won’t maximize your yield, but it spreads your income across genuinely different economic drivers.

The Tax Reality That Most Guides Skip

ETF dividend income is taxed differently depending on whether you’re in the US, UK, or Canada, and whether you’re holding inside a tax-advantaged account.

In the US, qualified dividends from stock ETFs held over 60 days are taxed at the lower capital gains rate (0%, 15%, or 20% depending on your bracket). Non-qualified dividends — which includes most bond ETF distributions and some REIT payouts — are taxed as ordinary income. If you’re in a 24% or 32% federal bracket, the after-tax yield on a bond ETF paying 4.5% can drop to roughly 3.1–3.4%. That changes the calculus.

UK investors receive a £500 annual dividend allowance (as of the 2024/25 tax year), with any dividends above that taxed at 8.75% for basic rate taxpayers and 33.75% for higher rate taxpayers. Using an ISA eliminates this entirely — income and gains inside an ISA are tax-free. For UK investors, holding income ETFs inside a Stocks and Shares ISA is almost always the most sensible structural decision.

Canadian investors holding US-listed ETFs in non-registered accounts face a 15% US withholding tax on dividends, though this can be recovered via the foreign tax credit. Holding the same ETF inside a RRSP eliminates withholding under the Canada-US tax treaty. The tax structure of the account you use matters as much as which ETFs you select.

This is an area where a conversation with a tax professional — not just a guide like this one — is worth having before you commit significant capital.

When the ETF Income Strategy Fails or Underperforms

There are conditions under which a passive income ETF strategy genuinely doesn’t work well, and it’s worth being direct about them.

Rising interest rate environments: When central banks are aggressively raising rates, bond ETFs lose capital value. Dividend equity ETFs often fall too, because higher risk-free rates make dividend yields relatively less attractive. If you hold long-duration bond ETFs without understanding rate sensitivity, your portfolio can drop 15–25% while still paying distributions leaving you with less than you started with.

Inflation outpacing distributions: A portfolio yielding 3.5% annually provides no real income if inflation is running at 4–5%. Your purchasing power is still declining. This isn’t a reason to avoid ETF income strategies, but it does mean yield alone is insufficient — the real yield (after inflation) is what matters for retirement planning.

Chasing yield into poor-quality funds: This is perhaps the most common failure pattern. A beginner finds an 11% yield fund and allocates heavily. Eighteen months later, the share price has erased more in capital than was ever collected in distributions. There are legitimate ETFs in the high-yield space, but they require careful analysis of distribution history, net asset value trends, and underlying holdings. The yield number alone tells you almost nothing about whether the fund is sustainable.

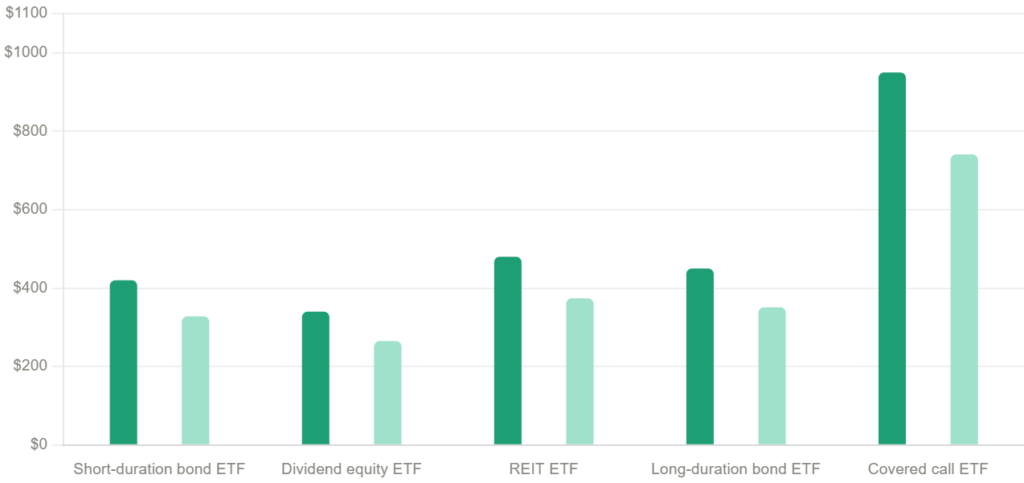

$10,000 Invested: What Income Looks Like Across Strategies

This second chart shows the approximate annual income generated by a $10,000 investment across different ETF types, assuming typical yield ranges and after accounting for a simplified tax drag at the 22% bracket (US) or basic rate (UK/Canada).

What this chart makes clear is that on $10,000, even the highest-yielding ETF strategy produces under $750 per year after a simplified tax drag. This is not a criticism of ETF income investing — it’s a reminder that scale matters enormously. Passive income from ETFs becomes genuinely meaningful at $100,000, $250,000, or above. At lower balances, the real value is in building the habit and the portfolio structure, not in living off the distributions.

Two Myths Worth Challenging Directly

Myth 1: High yield means better income. This is the most persistent misconception in this space. Yield is a ratio, not an amount — and the denominator (share price) can be falling while the numerator (distribution) stays artificially high. A fund whose share price has dropped 30% over three years while paying a 10% yield has actually destroyed capital. Total return — income plus capital change — is the only honest metric.

Myth 2: ETFs are set-and-forget forever. This is partly true for broad index funds held for capital growth, but less true for income-focused ETFs. Distribution policies change. Funds alter their holdings. Interest rate environments shift. REIT ETFs behave very differently depending on the property sector composition and leverage of underlying trusts. Checking your income ETFs once or twice a year, reviewing the distribution history, and confirming the NAV hasn’t been quietly declining over 12–24 months — that’s a reasonable minimum level of attention. Passive doesn’t mean uninformed.

What to Check Before You Buy Any Income ETF

The expense ratio matters more than people think at scale. A 0.65% annual fee on a fund yielding 3.8% is meaningfully eating into your net return — you’re receiving 3.15% effectively. Comparable ETFs in many categories are available at 0.07%–0.20% expense ratios. There’s rarely a good reason to pay significantly more.

Look at the distribution history over at least three years. A fund with steady or growing distributions is a different animal than one whose payout has been declining quarterly. The fund company’s investor relations page or the fund factsheet will show this clearly. For US investors, sources like the SEC’s EDGAR database can verify fund filings. For UK funds, the fund prospectus filed with the FCA is the authoritative document.

Check what’s actually inside the ETF. A “dividend income” ETF that holds 15% financials and 12% energy might behave very differently from one concentrated in utilities and consumer staples during a recession. The top 10 holdings and sector allocation should be in the fund’s fact sheet and take under five minutes to review.

Finally: don’t hold high-yielding income ETFs in a taxable account if you have tax-advantaged space available. The compounding benefit of sheltering distributions from annual taxation over 10–20 years is substantial, and it’s one of the clearest free advantages available to investors in the US (IRA, 401k), UK (ISA, SIPP), and Canada (RRSP, TFSA).

FAQs

Can you really live off ETF dividends?

Yes, but the capital requirement is larger than most guides imply. To generate $3,000/month ($36,000/year) from ETF dividends at a realistic 3.5% yield, you’d need roughly $1,030,000 invested before taxes. At 4.5%, you’d need around $800,000. This is achievable as a long-term goal but not realistic as a near-term income replacement for most people.

Are dividend ETFs safer than individual dividend stocks?

In terms of single-company default risk, yes — diversification across 50–500 companies means one bad earnings report won’t crater your income. But ETFs can still lose capital value, and they don’t eliminate sector risk. A dividend ETF heavily weighted in banks, for example, will still suffer significantly in a financial sector downturn.

What’s the difference between distributing and accumulating ETFs?

A distributing ETF pays dividends out to you as cash. An accumulating ETF automatically reinvests those dividends inside the fund, increasing the share price instead. For income investors who want regular payments, distributing is the appropriate choice. Accumulating versions are better for growth-focused investors who don’t need current income and want to defer taxable events.

How often do ETFs pay income?

It varies by fund. Some pay monthly (common with bond ETFs and covered call ETFs targeting income investors), others quarterly (most dividend equity ETFs), and some annually (common with certain accumulating funds converted to distributing mode). Monthly payers are often preferred by investors managing living expenses, but the frequency itself doesn’t affect the total annual return.

Is now a good time to invest in income ETFs given current interest rates?

The rate environment matters significantly. When rates are high relative to historical norms, bond ETFs become more competitive against dividend stocks for income. The risk is that if rates fall, bond ETF prices rise (a benefit), but future distributions may decline as older higher-yielding bonds mature and are replaced with lower-yielding ones. There’s no universally correct answer — it depends on your timeline, tax situation, and whether you’re prioritizing current income or total return.

Should a beginner start with one ETF or multiple?

Starting with one broad ETF is a reasonable approach if you’re still learning and don’t yet have the knowledge to evaluate multiple funds independently. A single diversified dividend equity ETF or a short-duration bond ETF gives you real-world experience of how these vehicles behave before you start layering complexity. Adding a second or third fund when you have a clear reason for the diversification — not just because more seems better — is the sensible progression.

")

")

[…] How to Invest in ETFs for Passive Income […]

[…] How to Invest in ETFs for Passive Income (Beginner Strategy) […]