Starting with a small amount feels like a disadvantage until you realize that most people who built serious portfolios didn’t start with serious money. The real problem isn’t the amount — it’s putting $500 into one stock because it looked promising, watching it drop 40 percent, and then avoiding investing altogether for the next three years. That’s the mistake that actually costs people.

Diversification with limited capital is genuinely possible, but the way most beginners approach it creates a false sense of security. Owning five tech stocks isn’t diversification. Owning an S&P 500 index fund and calling it diversified because it holds 500 companies ignores the fact that the top ten holdings make up nearly 30 percent of the fund’s weight. These distinctions matter when markets move against you.

Why Small Investors Get Diversification Wrong

The conventional advice is to spread your money across different assets. That’s directionally correct but practically incomplete. A portfolio of $1,000 split across ten individual stocks means $100 per position — too small to absorb any meaningful upside and still exposed to full downside on any single name.

The Illusion of Diversification

Owning multiple assets that move together in a crisis isn’t diversification. In March 2020, nearly every asset class dropped simultaneously — stocks, REITs, corporate bonds, and commodities all fell within weeks of each other. The only things that held were US Treasury bonds and cash. A beginner investor who thought they were diversified across stocks and real estate investment trusts learned that correlation spikes exactly when you need protection most.

True diversification means holding assets that respond differently to the same economic event. That’s harder to achieve than it sounds, and with limited capital, you have to be deliberate about it.

The Cost Problem No One Mentions

Ten years ago, building a diversified portfolio with small amounts was genuinely difficult because transaction costs ate into returns. That’s largely gone now with commission-free brokers. But a subtler cost problem remains — tax drag, fund expense ratios, and the opportunity cost of holding too much cash while waiting to deploy it gradually.

A $200 monthly investment split across six different ETFs generates more complexity than benefit at that scale. Two or three well-chosen funds can cover more ground with less friction.

What Actually Counts as Diversification

Before deciding how to allocate, it helps to understand what you’re actually diversifying across. There are four dimensions worth thinking about:

Asset class — stocks, bonds, real estate, commodities, cash. Each behaves differently across economic cycles.

Geography — US markets have outperformed internationally for over a decade, but that won’t hold indefinitely. Concentration in a single country adds political and currency risk that most small investors ignore.

Sector — technology, healthcare, energy, financials, consumer staples. Sectors rotate in and out of favor based on interest rates, inflation, and growth expectations.

Time — this one gets overlooked. Holding assets with different maturity profiles — short-term bonds alongside long-term equity — creates a form of diversification across your own investment horizon.

With limited money, you can’t cover all four dimensions perfectly. The goal is reasonable coverage across the most important ones without overcomplicating the structure.

Building the Portfolio: A Practical Starting Point

This isn’t a model portfolio — it’s a framework. Your specific situation, tax position, and timeline matter. What works for someone in their late twenties with stable income looks different from someone in their forties with irregular cash flow.

The Core: Low-Cost Index Funds

For most small investors, two or three broad index funds cover the essential ground. A total US market fund, an international developed market fund, and a bond fund of intermediate duration gives you exposure to thousands of securities across multiple geographies and asset classes for a combined expense ratio that often sits below 0.10 percent annually.

This isn’t exciting. It’s also not supposed to be. The point of the core is stability and broad participation, not outperformance.

The ratio between these funds depends on your timeline and risk tolerance. Someone with 20-plus years before they need the money can hold a higher equity allocation. Someone within five to seven years of a major goal — a house purchase, retirement — needs more in bonds and stable assets regardless of how confident they feel about markets.

Adding Real Exposure Without Buying Property

Real estate belongs in a diversified portfolio, but buying physical property with limited capital means concentration, leverage, and illiquidity. A REIT ETF gives you exposure to commercial real estate, residential, industrial, and healthcare properties across hundreds of underlying holdings for the price of a single share.

REITs behave differently from broad equities in certain environments — they tend to struggle when interest rates rise quickly, which matters in the current rate environment, but they also provide income that equity-heavy portfolios often lack.

I wouldn’t overweight REITs with small capital. Five to ten percent of a small portfolio is enough to add meaningful diversification without creating sensitivity to a single sector.

The Role of Bonds When Rates Are High

Bonds get dismissed by younger investors because they’ve underperformed equities over long periods. That’s true but incomplete. The function of bonds in a portfolio isn’t to generate equity-like returns — it’s to reduce volatility and provide something to rebalance from when equities fall.

When bond yields are higher, as they have been since 2022, the case for holding some fixed income improves. A short-duration bond fund earning four to five percent with minimal price volatility serves a different purpose than a long-duration fund that moves significantly with rate expectations.

This only works if you actually rebalance. Holding bonds that appreciate while equities fall and then selling bonds to buy equities at lower prices is how diversification generates real returns over time. Investors who hold both but never rebalance miss most of that benefit.

When This Strategy Underperforms or Fails

Diversification with index funds will consistently underperform a concentrated bet on the right sector during a bull market. From 2010 to 2021, a portfolio heavy in US technology significantly outperformed a globally diversified portfolio. Anyone who stuck with diversification during that period looked wrong for a long time.

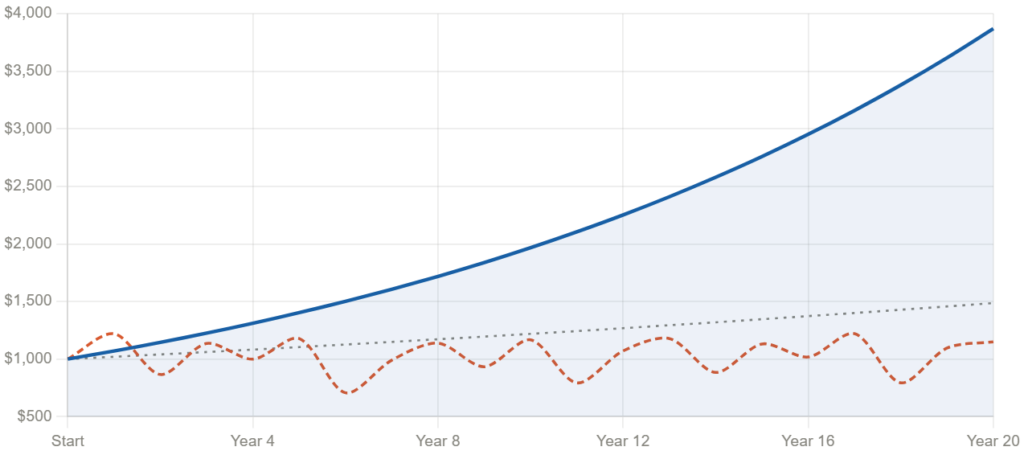

The Patience Problem

This is where most small investors abandon the strategy. Watching a concentrated position in something like semiconductor stocks outperform your balanced portfolio by 30 percent in a single year is genuinely difficult. The temptation to chase that performance is understandable and usually expensive.

Diversification works over full market cycles, not calendar years. The investors who benefited most from it are the ones who held through periods when it looked like a losing approach.

When You Have Too Little to Diversify Meaningfully

Below a certain threshold — roughly $500 to $1,000 — the practical case for diversification weakens. Transaction complexity, potential tax events from rebalancing, and the mental overhead of managing multiple positions can outweigh the benefit.

At that scale, a single broad market fund and a cash position is a more honest starting point. Add complexity as the portfolio grows, not before.

Two Myths Worth Addressing Directly

“You need to time the market to build wealth with small amounts.”

The math on this is clear. Missing the ten best trading days in any given decade dramatically reduces long-term returns. Most of those days happen during or immediately after periods of maximum fear, when individual investors are most likely to be sitting in cash. Consistent investment regardless of market conditions outperforms most attempts at timing across long horizons.

“More assets always means more diversification.”

Holding 15 ETFs creates administrative complexity without proportional risk reduction. Beyond a certain point — roughly five to seven uncorrelated positions — adding more holdings produces diminishing diversification benefit. The correlation between a 12-fund portfolio and a 4-fund portfolio is often surprisingly high, while the former requires significantly more attention to rebalance correctly.

The Tax Dimension Small Investors Ignore

In the US, UK, and Canada, the account type you use matters as much as what you hold. A diversified portfolio held in a taxable brokerage account generates annual tax events from dividends and rebalancing. The same portfolio held in a Roth IRA, ISA, or TFSA grows without that drag.

Small investors should max available tax-advantaged accounts before building taxable positions. The compounding difference over 20 years between a taxable and tax-sheltered account is substantial — often more impactful than the specific funds chosen.

This is one area where getting advice from a fee-only financial advisor, even for a single session, can pay for itself many times over. The IRS, HMRC, and CRA each publish guidance on contribution limits and eligible account types that’s worth reading before making decisions.

Frequently Asked Questions

How much money do I need to start a diversified portfolio?

Practically, $500 is enough to open a position in a broad index fund with most commission-free brokers. Meaningful diversification across multiple asset classes becomes easier around $2,000 to $5,000. Below $500, focus on a single broad market fund and build from there rather than spreading too thin across multiple positions.

Is it better to invest a lump sum or spread it out monthly?

Research consistently shows that lump sum investing outperforms dollar-cost averaging roughly two-thirds of the time over long periods, simply because markets tend to rise over time and staying invested captures more of that. The honest reason most people use monthly contributions isn’t optimization — it’s that they don’t have a lump sum available. Both approaches work. The one you’ll actually stick to is the right one.

Should I include cryptocurrency in a diversified portfolio?

Cryptocurrency has a low correlation with traditional assets in normal markets, which is the technical argument for including it. The problem is that during stress events, that correlation rises significantly — exactly when you need diversification to work. A small allocation of two to five percent won’t meaningfully hurt a portfolio, but it also won’t save it. If you hold crypto, do it with money you can genuinely afford to lose entirely, not as a core diversification tool.

How often should I rebalance with a small portfolio?

Annual rebalancing is sufficient for most small portfolios. More frequent rebalancing generates unnecessary tax events in taxable accounts and produces minimal additional benefit. A reasonable trigger is rebalancing when any single position drifts more than five percentage points from its target allocation, or once per year — whichever comes first.

What’s the biggest mistake small investors make with diversification?

Confusing activity with strategy. Buying and selling different funds in response to news, rotating between sectors based on short-term performance, or constantly adjusting allocations based on what worked last quarter — all of these feel like active portfolio management but statistically underperform a static, low-cost allocation held consistently over time. The discipline to stay with a boring portfolio during exciting markets is underrated and genuinely difficult.

What to Check Before You Invest a Single Dollar

Look at the expense ratio of every fund you’re considering. Anything above 0.50 percent annually requires a specific justification — most broad index funds cost a fraction of that. Check whether you’re using the most tax-efficient account available to you before opening a taxable position.

Avoid building a portfolio around recent performance. The sectors and geographies that led last cycle rarely lead the next one. A portfolio constructed from last year’s winners tends to be last year’s portfolio — not next year’s.

The decision in front of you is simpler than it feels. Choose two or three low-cost funds that cover different asset classes and geographies, set up automatic monthly contributions, and commit to annual rebalancing. The complexity can come later, when the portfolio is large enough to justify it.